“The Metamorphosis,” written by Franz Kafka, is a profound and unsettling tale that begins with its protagonist, Gregor Samsa, awaking to find himself transformed into a large, grotesque insect-like creature.

Gregor, initially bewildered and disoriented, tries to continue with his normal, routine, life. He struggles to adjust to his new, unwieldy body and the alienation it brings. His physical transformation becomes a barrier to his work and social life, as he can no longer support his family through his job as a traveling salesman. This change in Gregor is not just physical but also deeply psychological and emotional. He becomes increasingly isolated and estranged from his family, who are unable to accept his new form.

The story delves into the reactions of Gregor’s family members, who are shocked, horrified, and eventually repulsed by his transformation. As the story progresses, Gregor becomes a source of shame and financial burden for his family. Gregor’s existence becomes increasingly pitiful and confined. He is left to languish in his room, hidden away from the world, his human thoughts and emotions trapped within a monstrous body.

Kafka’s work, with its blend of the surreal and the mundane, provides a rich allegorical context to explore the transformative impact of fiscal and monetary policy decisions that have led to challenging capital market conditions over the past 3 years.

Much like Gregor, economic policymakers are facing an identity crisis and capital markets reflect this. Although reconciliation was impossible for Gregor, policy makers and investors must navigate together the painful and transformative effects of inflation and the normalization of interest rates to restore equilibrium in capital markets and reverse inflation’s metamorphosis of the financial landscape.

An Extraordinary Triennium

The past three years, in the wake of the global pandemic, have produced some of the most extreme conditions for capital markets since the Great Depression. One might ask, “How can this be with 4.5% unemployment and only a mere recessionary blip?” Fair enough, that is a valid question. However, that question and others like it underscore a critically important lesson—economic crises are not the same as financial crises.

Let’s consider the labor market which is often used as a direct indicator of economic health. Currently, the U.S. workforce is aging and both the labor force participation rate and the demand for labor are in decline. The current labor force participation rate of 62.7% is the lowest since January 1978. The current population dependency ratio—the population of older dependents relative to the working-age population—is the highest of the past 63 years at 26%.

Despite this, labor markets are currently considered strong by conventional measures. Unemployment is low and personal incomes and labor productivity are both on the rise. It comes as no surprise that economists are not lining up to forecast deep economic recessions while unemployment squats around 3.9%.

The past three years have demonstrated, as clearly as ever, that financial and economic crises can be asynchronous. Policy responses to the economic crisis precipitated by the global pandemic continue to reverberate through capital markets. Quite frankly, no investor has been entirely safe.

John F. Kennedy is famously quoted as saying, “A rising tide lifts all boats.” However, in this post-pandemic triennia in which inflation eroded consumer purchasing power by 15%, the real (adjusted for inflation) annualized return of the NASDAQ composite was -1.96% per year, and the US Aggregate Bond Index was down a cumulative 18%—it might be more accurate to say, “A rising tide lifts all boats, but too much cheap money and inflation will do their best to sink them.”

Financial Crises, Identity Crises

Today’s markets present a study in contrasts. Over the past 12 months ending October 31st, the S&P 500 index grew by 19%. During this same period, the seven largest stocks in the S&P 500, now dubbed the “magnificent seven”, increased by 71%. The remaining 493 stocks increased only by 6%.

Even more shocking, the US Aggregate Bond Index is teetering on the brink of its third consecutive year of losses—a scenario unseen in at least the last four decades. The index decreased in value by -1.8% and -13.1% in 2021 and 2022, respectively, and is currently up about 2.39% year-to-date in 2023. The decline in 2022 represents the index’s steepest drop in more than 40 years.

A variety of explanations have been put forth to justify these extraordinary capital market experiences ranging from a decline in global business competitiveness, low worker morale, and lackluster earnings guidance all the way to far-reaching geopolitical tensions with monumental economic implications.

But let’s be clear, the extraordinary investor experience over the past three years is too extreme to warrant explanations based merely on correlation. To understand where we are and where we are going, we must focus on causation. The cause for this extreme investor experience is clear: the hazards of cheap money, chiefly inflation, and the effects of bond convexity in low interest rate environment—which is a complicated way of saying the penalty of a 5% hike in interest rates on a bond yielding 0.50% is 25% worse than penalty of an identical 5% hike in interest rates on a bond yielding 5%.

Inflation’s Transformative Effects on the Crisis Playbook

Since the turn of the millennium, the U.S. has navigated three major economic upheavals: the Dot.com bust, the 2008 financial meltdown, and the recent Covid-19 crisis. Each time, economic policymakers have leaned on a familiar strategy: monetary stimulus, notably quantitative easing, to stabilize markets, and fiscal injections to bolster consumer confidence. This approach proved effective during the first two crises but faltered in the wake of the pandemic.

Entering the pandemic, the Fed was already grappling with lower policy rates, and the pandemic’s impact on employment and productivity, though severe, was fleeting compared to previous crises. History has demonstrated that the pandemic’s fiscal response, while well-intentioned, was excessive and ignited a surge of inflation that has proven costly to investors, particularly fixed income investors.

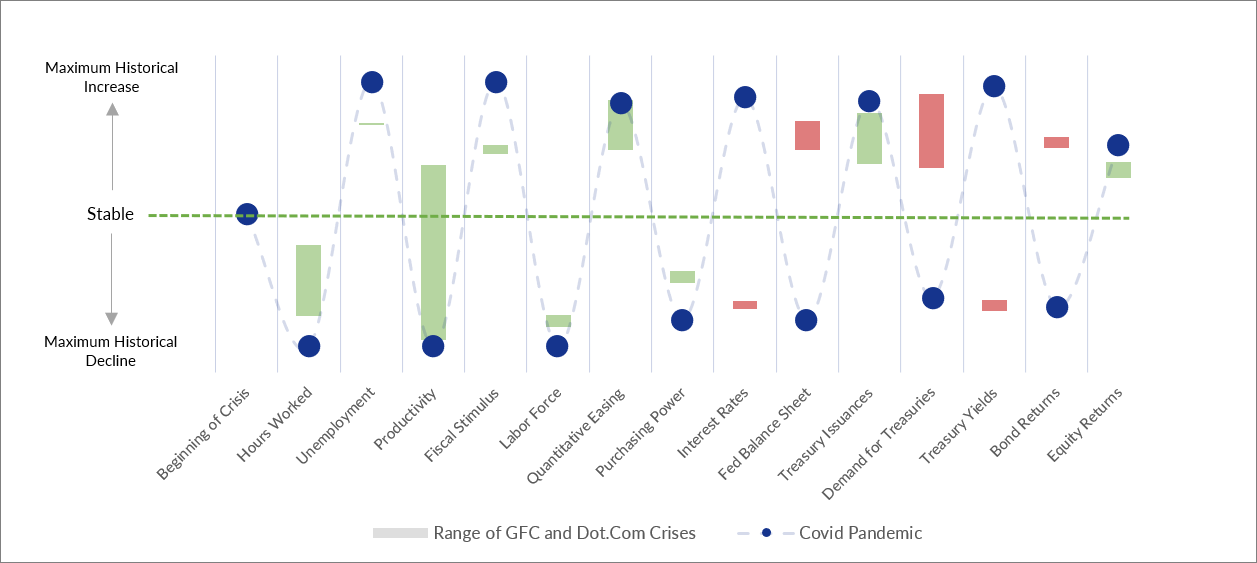

An illustrative chart details this pattern: the magnitude of crises and policy responses over time. Each blue dot marks the Covid-19 crisis’s impact, set against the backdrop of the range of the Dot.com and 2008 crises shown in red and green rectangles. The height of each wave indicates historical significance of each event relative to history. For instance, the pandemic’s unemployment spike, unprecedented in speed and scale, reaches the chart’s peak. Meanwhile, treasury demand post-pandemic slowed, a stark contrast to the increases in treasury demand seen in previous downturns, represented by the red rectangles.

Historical Extremity

During the pandemic, the U.S. experienced historic labor market disruption: unprecedented drops in demand and productivity, the fastest rise in unemployment, and massive fiscal and monetary stimuli. The policy response, though initially mirroring past crises, quickly diverged due to soaring inflation. The Federal Reserve was forced to abandon its proven crisis playbook, and shifted toward a strategy of quantitative tightening. Interest rates skyrocketed to 5.25-5.50% in just 16 months, and the Fed reduced its balance sheet by $1.1 trillion.

Amidst these shifts, the Treasury faces a nearly -$1.7 trillion deficit in 2023, leading to massive debt issuance, which is occurring at a time when the treasury market is relying less upon the Fed and foreign investors and more on private domestic investors. Declining demand for Treasuries has the potential to raise market yields higher, which inversely impacts bond prices causing them to decline. Combined, this tension led to significant market downturns, including a -13% drop in the Aggregate Bond Index in 2022.

The Fed now confronts a dilemma: stabilizing inflation at the risk of causing economic decline versus stimulating the economy and risking a reignition of inflation and its powerfully corrosive effects. Traditional tools like rate cuts are less viable, constraining the Fed’s response to stagnation and inflation. This uncertainty impacts consumer spending and investor confidence, complicating economic recovery.

This scenario suggests the U.S. is in proximity to a deleveraging cycle, in which markets may be adjusting disparities between interest rates, market operations, treasury issuance and demand, and yields. Fixed income investors already feel a significant impact because of this, while equity investors are likely to remain heavily dependent on the Fed’s decision-making.

Conclusion

After a year of relative caution in which we held modest cash positions and maintained a disciplined focus on high-quality assets across fixed income and equity categories, we’re preparing to re-engage with fixed income asset classes and continue our focus on quality fixed income and equity investments.

Fixed-income securities have grown more attractive. Thanks to higher interest rates, their returns are more enticing. What has been a challenging environment for debt holders has transformed into a more opportune environment for new debt investors or existing debt investors seeking to deploy additional capital. Since the Federal Reserve’s policy rate has approached the higher end of their stated target policy range, volatility stemming from interest rate fluctuations is expected to offer more upside potential than downside potential moving forward. We will be looking for opportunities to increase quality through higher allocations to government debt securities.

For equities, our focus remains on quality: companies with healthy balance sheets, strong cash flows and meaningful competitive advantages. We anticipate a challenging environment for Real Estate investments and will be focusing more on globally diversified opportunities across developed markets as part of our continued focus on holding quality assets.

In addition, we are preparing a new growth-focused allocation tailored to clients with longer, clearly defined, investment horizons. That approach will aim to harness “next-gen” growth trends expected to unfold over the next 10-20 years and would be most suitable for what we view as our next generation of American Trust Wealth clients.

The current market presents a balancing act between risks—like potential volatility and policy shifts—and opportunities, especially in innovative sectors or undervalued assets. Despite uncertainties, market history teaches us resilience and adaptability. This means focusing on the intersection of what we can control and what is most important to us.

We urge clients to regularly review their liquidity needs and keep lines of communication open, helping us to ensure portfolios are shaped according to their immediate and future needs. We foresee a return to stability despite the post-pandemic tremors that still reverberate through markets.

Our commitment is to guide you through these times with proactive planning and clear communication. Our team stands ready to assist in updating and adapting your financial strategy, positioning you for both current challenges and future growth. Your trust in our partnership is invaluable. As always, please do not hesitate to reach out to your Fiduciary Investment Advisor with any questions or concerns you may have.