When two worlds collide, there is bound to be a spectacle. This past weekend, Cincinnati experienced such a collision as the city teemed with an influx of music and sports enthusiasts. The city, already known for its love of baseball, was not just painted red by Cincinnati Reds fans eager to see rookie phenom Elly De La Cruz dazzle sellout crowds, it also experienced a unique shade of pop culture red as Swifties descended on the town for the highly anticipated Taylor Swift concerts. Swifties, the dedicated fan base of pop superstar Taylor Swift, along with baseball and soccer fans, added an estimated 130,000 people to the typical commuter’s already filling the city streets during Friday evening rush hour.

The crowds, however, were not the only spectacular force last weekend. The socioeconomic impact of the pop superstar’s concert tour, along with concurrent Reds and FC Cincinnati games, were themselves spectacular. It is estimated that the economic impact of Swift’s Eras Tour will be nearly $50 million dollars in Cincinnati alone. Factoring in the additional effect of baseball and soccer fans, the total impact may be as high as $90 million. In fact, Swift’s concerts are having a demonstrable impact on the GDP of 20 localized economies nationwide. Media observers are affectionately referring to this effect as the “Taylor Swift Economy”, and the ripple effect of Swift’s fandom has sparked discussions around ‘Swift-flation’, a term which came to life as economic activity around these events surged.

While it may seem trivial or even humorous, these instances reflect the myriad factors that come into play in our complex economic ecosystem. In a broader context, the economic impact of concert tours is relatively de minimis, however, one cannot overlook the average Eras Tour concertgoer’s current penchant for consumption—particularly in this economic landscape. Price levels remain a critical concern for the Federal Reserve as it navigates monetary policy through an inflationary environment which remains elevated above the Fed’s long-term inflation target rate of two percent.

An Update on Price Levels

Inflation pressures in the U.S. showed signs of easing in May as aggregate consumer spending slowed. The core personal consumption expenditures (PCE) price index, a key indicator monitored by the Federal Reserve, increased 0.3% for the month, matching analyst expectations. The year-on-year core PCE grew by 4.6%, slightly less than expected. When including volatile food and energy components, inflation was softer, rising just 0.1% for the month and 3.8% from a year ago. Economists suggest that consumers are nearing the end of their spending spree as most of the pent-up demand has been released.

While inflation is gradually moving in the desired direction, it remains above the Federal Reserve’s 2% long-term target policy. Fed officials anticipate at least two more quarter-point interest rate hikes by the end of the year to control inflation and traders anticipate an 83% probability of a quarter-point hike at the July Fed meeting. As prices have risen, consumers have reduced their pace of spending and increased savings, pushing the personal savings rate for May up to 4.6% from 4.3% in April. Spending has also begun shifting back towards services, reversing the pandemic trend of consumers gravitating towards higher-priced goods.

Consumer Price Dynamics

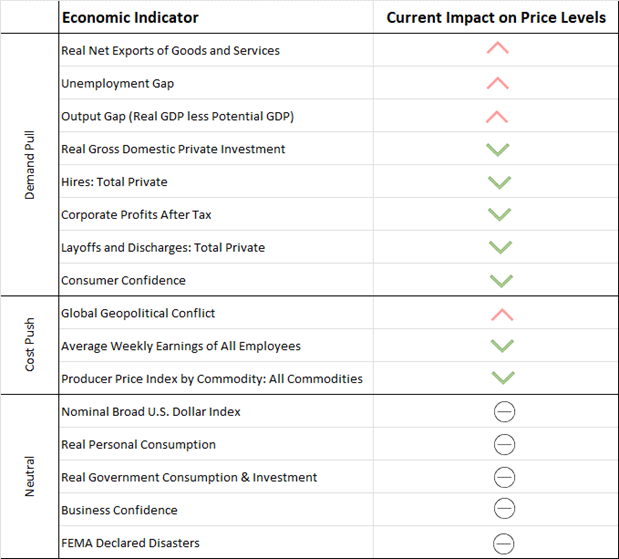

Last November we discussed the different types of inflation (Cost-push and Demand-pull) along with the impact of more than a dozen variables that drive those types of inflation. Below is an updated summary of the impact each variable is currently having on inflation. The variables are grouped by the type of inflation. Red arrows demonstrate that a variable is currently exerting inflationary pressure on prices, whereas green arrows demonstrate that a variable is currently providing relief to inflationary pressure.

Inflation and Interest Rate Outlook

Consistent with indicators presented last Fall, inflationary pressures have subsided in 2023. Current indicators are predominantly pointing toward disinflationary pressures across both demand-pull and cost-push variable categories.

As far as demand-pull indicators are concerned, the unemployment gap and output gap present the most inflationary potential. Unemployment remains below the natural rate of unemployment which means a competitive labor market could continue to drive wages up which could increase demand and consumer prices. That said, wage growth has slowed substantially. The output gap is the difference between real GDP and potential GDP. With real GDP below potential GDP, this indicates there is available productive capacity across the economy and along with it the potential for added economic growth. Economic growth increases aggregate demand and puts pressure on consumer prices.

However, most factors are either disinflationary, deflationary, or neutral, meaning they are not putting inflationary pressure on consumer prices. Corporate profits, new hires, and both consumer and business confidence levels are all below average. Corporate layoffs remain above average. A decline in the growth of production input costs as measured by the Producer Price Index (PPI) also indicates less pressure on consumer prices.

Despite this, Federal Reserve Chair Jerome Powell has recently affirmed that it is sensible to continue moderating the pace of interest-rate increases. This follows the most recent rate hike in May, which saw interest rates rise to between 5% and 5.25%, a 16-year high. Powell has hinted that rates may rise again during the Fed’s July meeting. The central bank’s goal isn’t a specific number of rate hikes, but a policy stance that helps manage inflation to around 2%. The past year has seen aggressive rate increases, including four consecutive hikes between June and November. However, the pace of these increases has since slowed.

Powell noted that holding rates steady in the current month could further moderate the pace of increases. The chair expressed that while most Fed officials projected at least two more hikes this year, the final decision will be data dependent. In an era of low interest rates and inflation, a 5% short-term interest rate might have seemed improbable, but it’s now being considered a potentially ‘tight’ policy to help manage inflation.

‘Karma’, a Relaxing Thought?

On her most recent album, Taylor Swift shares some open views on the topic of karma. In the investment management world, we have recently spoken of the investor experience in 2022 as a great reset from the mid and post-pandemic monetary and fiscal stimulus and the karmic wave of inflation that followed. Although painful at times, the experience in 2022 did at least provide some rationalization within markets one may fairly describe as, if not relaxing, perhaps reassuring. Current levels of corporate profits, new hires, and consumer and business confidence, while lower than average, are showing signs of improvement and present opportunities for selective investments in markets that are poised for recovery. While the possibility that the Federal Reserve may continue to increase interest rates is on the table, we remain flexible and view fixed income asset classes as prime candidates for a tilt toward active management when prudent. We stand prepared to adjust our portfolio strategy based on real-time data and trends as they develop.

We remain cautiously optimistic concerning the outlook for the second half of 2023 as capital markets weigh the cause and effect of the Fed’s tightening monetary policy. Today’s markets are as dynamic and complex as ever, so it is our privilege to partner with you to help guide you toward achieving your goals. As always, if you have any questions, please don’t hesitate to reach out to your Fiduciary Investment Advisor.

Products and services offered by American Trust Company are not insured by the FDIC, are not a deposit or other obligation of, or guaranteed by, American Trust Company, and are subject to investment risks, including possible loss of the principal amount invested.