The Federal Reserve just raised interest rates again. Inflation is on the rise. The unemployment rate remains low despite a recent wave of corporate layoffs. What does it all mean?

That is the quintessential investor question, and it is a difficult one to answer.

The first step to answering this question is to understand how truly complicated it is. A favorite book around the American Trust Wealth office is “Thinking, Fast and Slow” by Daniel Kahneman. The book is a treasure trove of insights and research on human psychology and decision-making. The book details how people often make errors in judgment and decision-making due to cognitive biases and heuristics that influence thought processes.

Some of the more prominent concepts discussed in the book are confirmation bias, availability bias, and substitution bias. Below are brief descriptions of each one:

- Availability Bias – The tendency to rely on readily available examples or information when making decisions, rather than seeking out more representative or accurate data.

- Confirmation Bias – The tendency to seek out information that confirms our existing beliefs and ignore information that contradicts them.

- Substitution Bias – The tendency to answer a difficult question by replacing it with a simpler, related question and answering it instead.

We see these biases displayed often in the news and popular media. Kahneman’s research alters the way one sees the world. Once you are familiar with the concepts they begin to appear everywhere. And, all too often, we may find that what we perceive as the best answers are sometimes the worst examples of these shortcuts.

Making Sense of It All

Investors absorb current events and economic data to inform decision-making processes, but it is natural to interpret the information in ways that are most relatable to us, personally.

As a society, Google News and Search trends reveal that prior to 2008 terms like “Dot.com bubble” or “tech bubble” were preferred metaphors for periods of economic and financial collapse, whereas in the wake of 2009, terms such as “global financial crisis” or “subprime crisis” emerged and replaced them. All these terms evoke strong emotions, influence our perception of current conditions, and at times, may even lead us to marginalize objective data.

In practice, we often observe thought processes that go something like this:

I nearly lost everything in the ‘dot.com bubble’ in 2001-2002 (availability bias).

It feels like we are on the verge of another bubble bursting, the stock market is so volatile right now (confirmation bias). Should we move risky assets to cash (substitution bias)?”

For this investor, availability bias occurs when the most recent or most severe financial crisis looms over our historical context. Confirmation bias occurs when we correlate that context to current conditions even when underlying conditions vary. And finally, substitution bias occurs when we replace difficult questions such as, “What opportunities does this market present?” or “What is the impact of current market conditions on my long-term financial plan?” with simpler questions like, “What are my potential losses if we experience another financial crisis?”

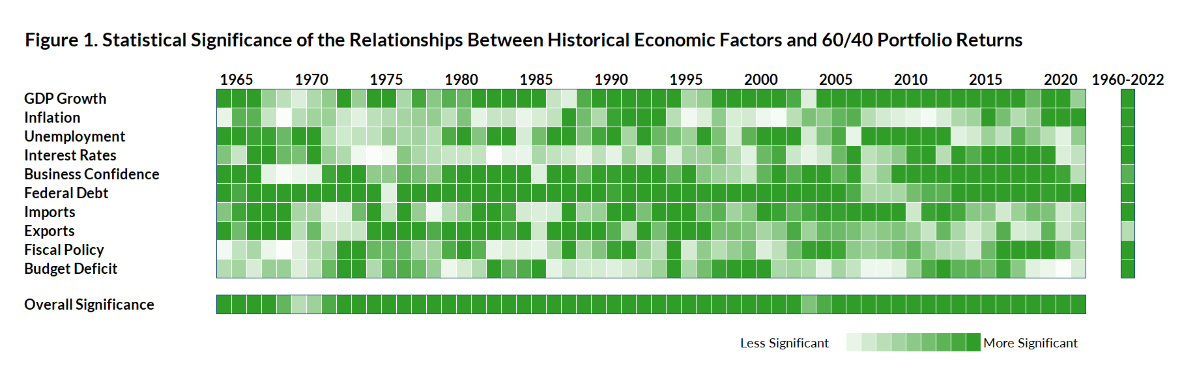

It is helpful for investors to maintain an informed and objective long-term historical awareness. Regression analysis is a statistical method for estimating how things relate to each other. To better inform our historical awareness, we used this technique to evaluate the significance of economic data over time and then measured the similarities between historical time periods and today. For purposes of this analysis, we used common economic indicators to explain the performance of the 60/40 asset allocation, which better reflects the average investor’s experience, compared to a true stock market index.

Figure 1. illustrates the relative significance of ten common economic indicators between 1965-2022 using a monthly rolling 5-year regression analysis beginning with data in 1960. Individually, the statistical significances vary substantially over time, however, the overall significance of these economic indicators is very strong. On average, these variables explain about 92% of the variation in 60/40 portfolio returns and at least 70% of the 60/40 performance in 99% of observation periods.

For example, the data reflects a very strong relationship between 60/40 returns and the growth of the Federal Debt between 1960-1975, GDP Growth (positive and negative) between 1991-2003, and the Unemployment Rate between 2001-2013. On the contrary, the data reflects weak relationships between the 60/40 portfolio return and Inflation between 1992-2002, the size and balance of the Fiscal Budget between 1960-1971, and volatile Interest Rates between 1968-1976.

Back to the Future

When we hear significant economic news, we immediately attempt to gauge the impact of the news. This is typically done by establishing context from historical precedents. The benefit of the analysis described above is that it instead helps provide an empirical basis for answering the question, “Which periods in history share the closest resemblance to today’s environment?”

Unlike Figure 1., which highlighted the revolving significance of economic indicators throughout history, Figure 2. instead compares the historical relationships between the economic data and 60/40 returns to today. So which time periods are closest matches to the past five years?

Statistically speaking, today’s economic conditions, and their recent relationship with the average investor experience, are most similar to the conditions in 2017, 1982, 1973, and 1995.

Below is a refresher of the economic conditions during each of those time periods:

- 2017 – There are strong similarities across the board between 2017 and 2022. GDP growth was fairly stable despite a slowdown in growth in 2015-2016, Unemployment was in steady decline from about 8% in 2013 to 4% in 2017, Interest Rates began to rise off 0% during 2016-2017 following a short stint of deflation in early 2015, the Fiscal Deficit was relatively stable, the Federal Debt expanded at an average rate of about 4.5% per year, and a brief decline in trade activity rebounded toward the end of the period. Between 2013-2017 the average annualized return of a 60/40 allocation was 8% per year. A 60/40 allocation returned about 0% in 2018.

- 1982 – The strongest similarities between 1982 and 2022 are seen in GDP, Fiscal Policy, Federal Debt, and Foreign Trade. GDP growth declined in 1980 during the first recession of the 1980s and then again between 1981-1982, the Federal Budget Deficit essentially doubled, Federal Debt expanded by more than 50%, and Foreign Trade was relatively stable but experienced a downward trend toward the end of the time period. Between 1978-1982 the average annualized return of a 60/40 allocation was 8% per year. A 60/40 allocation returned around 12% in 1983.

- 1973 – The strongest similarities between 1973 and 2022 are seen in Fiscal Policy, Foreign Trade, Interest Rates, Unemployment, and Inflation. Between 1969-1973 the Federal Budget went from a $3.2 billion surplus to a nearly $15 billion deficit, Exports grew by 20%, Interest Rates initially declined but then increased to nearly 11%, Unemployment was relatively stable around 5.5% following the recession in 1969-1970, and Inflation grew from an average around 4.5% between 1969-1972 to a high of nearly 9% in 1973. Between 1969-1973 the average annualized return of a 60/40 allocation was only 0.36%. A 60/40 allocation returned about -22% in 1974.

- 1995 – The strongest similarities between 1995 and 2022 are seen in Unemployment, GDP growth, and Foreign Trade. Between 1991-1995 Unemployment was declining to around 5.5% and GDP growth was relatively stable around 5.25% following the recession in 1990-1991. Growth in trade was strong at about 10% per year. Between 1991-1995 the average annualized return of a 60/40 allocation was 12% per year. A 60/40 allocation returned 11.5% in 1996.

Each of these time periods share significant similarities, both statistically and contextually. That said, there are some stark contextual differences within some of those correlations. For example, there were strong similarities between 1995 and 2022 regarding Fiscal Policy. The initial recovery of the Federal Budget Deficit in 2021 and 2022 following economic stimulus due to the Covid pandemic correlated closely with the reduction in deficit spending during the 1990s. This is also seen in the “reduction” of the Federal Debt growth rate in 2021 and 2022. Both of which, of course, arose very differently from the deficit and debt reduction efforts of the 1990s.

What Does It All Mean?

If it is not clear by now, we can state it plainly: there is no simple heuristic to answer this complex question, nor should you ever fall victim to one.

It is true that we set out with this analysis to demonstrate which eras in the past are most like current times, but we knew from the onset that we would accomplish something much more important: illustrating just how different eras are, how quickly conditions change, and the chaotic nature of short-term economic and financial markets.

Here is what we can reasonably say:

- Uncertainty Right Now is Rational – The overall explanatory power of these economic variables over more than five decades is very good. On average, they explain 92% of the variation in the 60/40 portfolio’s return between 1960-2022. That said, the statistical significance of these variables individually in 2022 is relatively weak. In fact, only Inflation and the Federal Debt are highly significant for the period 2018-2022. Inflation and its relationship with interest rates and unemployment are clearly a major concern for investors.

- Not That 70s Show – Investors are rightfully concerned about inflation, interest rates, and the potential effect on unemployment and productivity. Accommodative fiscal and monetary policies today are familiar to those in the 1970s and early 1980s. Inflation remains a clear and present risk to economic and financial markets that the Fed is managing carefully. That said, there are important differences between today and the 1970s:

- The Fed is managing inflation closely today. In May of 1971 a presenter to the FOMC stated that “cost-push” inflation was not within the influence of monetary policy. Cost increases were then viewed as a structural problem “not amenable to macro-economic measures.”

- The drivers of inflation during the 1970s are very different than today. In 1979, Fed Chairman Burns argued inflation was the result of a variety of forces: “The loose financing of the war in Vietnam…the devaluations of the dollar in 1971 and 1973, the worldwide economic boom of 1972-73, the crop failures and resulting surge in world food prices in 1974-75, and the extraordinary increases in oil prices and the sharp deceleration of productivity.” The US economy experienced monumental structural shifts during the 1970s. Since 1970, the purchasing power of the consumer dollar has declined nearly 90%. Of that decline, about 70% of it (a 61% decline) occurred between 1970-1982 alone.

- Our understanding of the relationship between inflation and unemployment is much better in 2022. During the 1960s and 1970s the belief was that higher inflation would lead to lower unemployment, however, the mid-1970s demonstrated that both inflation and unemployment could rise together. When it comes to inflation, interest rates, and unemployment, Ben Bernanke in 2004 explained that the decision to tighten or ease monetary policy ultimately depends on how policymakers balance the risks inherent in pursuing employment and price stability objectives. In 2023, the Fed is actively mounting efforts to maintain price stability and is doing so with unemployment still in decline around 3.4% as of January 2023.

- The Fed is managing inflation closely today. In May of 1971 a presenter to the FOMC stated that “cost-push” inflation was not within the influence of monetary policy. Cost increases were then viewed as a structural problem “not amenable to macro-economic measures.”

- Discipline is Paramount – The performance of the 60/40 portfolio during time periods matching closely to 2022 was mixed, but a clear theme emerges from history. The data certainly seems to suggest that the US economy may be currently undergoing a significant transition related to inflation and the federal debt, and it’s safe to assume the interest rate environment is playing a role in that. The experience for fixed income investors in 2022 was historically poor. Current times correlate highly with historical periods that were moving just beyond economic headwinds or were actively bridging periods of economic decline. The 60/40 portfolio returns in each year following 2017, 1982, 1973, and 1995 were 0%, 12%, -22%, and 11.5%, respectively. Since 1960, the average annual return of the 60/40 portfolio has been 6.3% per year.

This analysis allows us to demonstrate that we are truly in unique times and illuminates a wide range of potential outcomes for the remainder of 2023. That said, the need for a steadfast, disciplined, and unbiased approach to investing, anchored within proven financial planning and wealth management processes, remains as important as ever.

As always, if you have any questions, please don’t hesitate to reach out to your Fiduciary Investment Advisor. We are always here to help provide you with the answers to your difficult questions.

Products and services offered by American Trust Company are not insured by the FDIC, are not a deposit or other obligation of, or guaranteed by, American Trust Company, and are subject to investment risks, including possible loss of the principal amount invested.